Solana Decentralized Wireless(DeWi) Market Map

Everything you need to know about Solana DeWi Market in 2025

Introduction

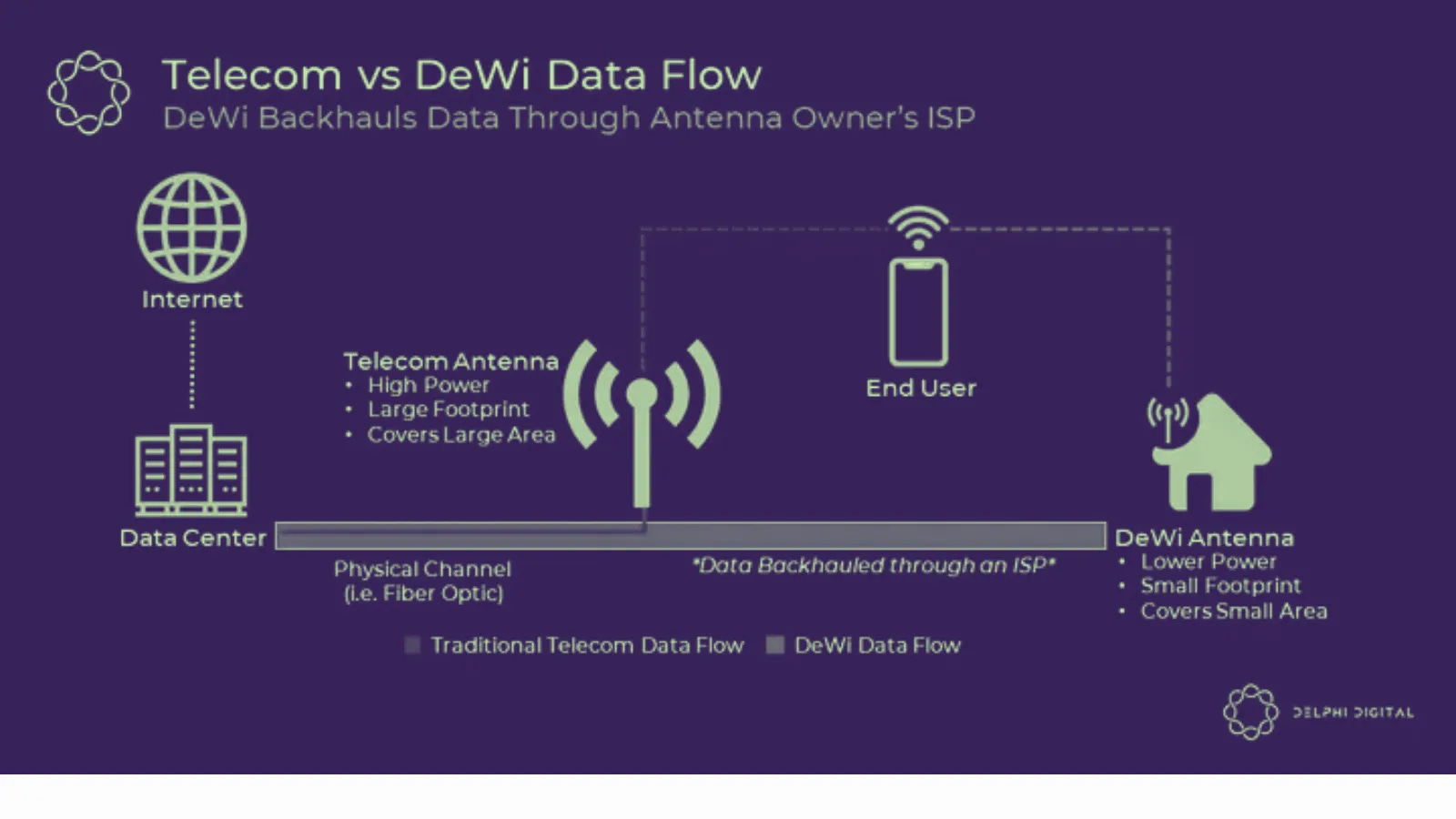

Decentralized Wireless (DeWi) revolutionizes telecommunications by using blockchain to coordinate community-deployed wireless infrastructure. Unlike traditional telecoms requiring massive capital investment and centralized control, DeWi allows individuals to earn crypto rewards for providing connectivity.

DeWi achieves superior economics through two key mechanisms: eliminating expensive spectrum licensing costs and implementing token-based incentives. This allows networks to expand into areas traditional telecoms find unprofitable.

As a key vertical within the broader Decentralized Physical Infrastructure Network (DePIN) ecosystem, DeWi focuses specifically on wireless connectivity, while DePIN encompasses storage, computing, and sensing networks.

Solana provides the ideal blockchain foundation for DeWi projects due to its high-throughput and low-cost transactions, essential when validating millions of connectivity proofs and efficiently distributing rewards.

The problem with traditional telecom and the opportunity for disruption

The telecommunications industry operates on a fundamentally centralized, capital-intensive model. Carriers must invest billions in spectrum licenses and infrastructure before generating revenue, naturally directing investment toward high-density areas with quicker returns. This creates a predictable pattern: excellent connectivity in urban centers alongside persistent gaps in rural and low-income areas.

The traditional deployment cycle repeats approximately every decade:

Securing significant debt financing for capital and operational expenditures

Acquiring spectrum licenses through government auctions

Procuring proprietary hardware from a limited set of manufacturers

Negotiating site acquisition with property owners

Deploying specialized technical personnel for installation and maintenance

The $2.46 trillion global telecom market is growing at 6.14% CAGR and projected to reach $4.21 trillion by 2034, yet faces challenges from customer dissatisfaction(low NPS) to increasing data demand.

As 5G and emerging 6G technologies require exponentially more infrastructure (5G and 6G use higher frequency spectrum which cannot travel as far or penetrate obstacles, requiring significantly more cell sites to cover the same area as 4G), traditional deployment economics are becoming unsustainable, especially in less profitable markets.

Decentralized wireless (DeWi) networks offer an alternative by distributing infrastructure ownership across thousands of participants using token-based incentives. This approach enables permissionless participation, lowers capital requirements, and promotes organic network expansion based on actual needs rather than projected ROI.

DeWi hasn't replaced traditional networks, but a complementary ecosystem is emerging. Decentralized networks are addressing specific gaps in conventional coverage, particularly in underserved areas and offloading data traffic in high-demand areas. This symbiotic relationship represents a significant improvement in efficiency in global connectivity that deserves attention from all market participants.

Why DeWi Now?

Several converging forces have created the perfect environment for DeWi to flourish:

eSIM Revolution: Mainstream eSIM adoption reduces carrier switching costs to near-zero, enabling seamless dual-network utilization.

Hardware Accessibility: Affordable, plug-and-play hardware simplifies network participation for non-technical users.

Spectrum Liberalization: Newly opened wireless spectrum bands like CBRS allow new market entrants to deploy networks without billion-dollar license acquisitions.

Blockchain Maturity: Cryptoeconomic protocols enable large-scale coordination through incentive structures previously impossible.

AI-Driven Optimization: AI algorithms optimize network performance in real-time, allowing distributed DeWi infrastructure to deliver comparable performance to traditional carriers.

How the DeWi Economic Flywheel Works

DeWi networks utilize a token-based incentive system that enables network bootstrapping without centralized coordination. This economic flywheel operates through four key phases:

Initial Hardware Deployment: Operators receive token rewards for deploying network hardware, providing an immediate return on investment and building critical infrastructure before usage fees are sustainable.

Network Growth Acceleration: Expanding coverage attracts additional operators. Token subsidies enable lower data transfer costs compared to traditional telecoms, drawing initial end users to the network.

Usage Revenue Generation: As coverage reaches critical mass, end users begin paying for data transmission. Operators earn dual revenue: ongoing token rewards plus usage fees.

Value Capture & Reinforcement: Networks employ either burn-and-mint equilibrium or work-token models. Token utility increases as supply is burned or staked, rising token value attracts more operators, and a virtuous cycle of growth becomes self-sustaining.

This mechanism effectively solves the cold start problem that plagues network-based businesses. By incentivizing supply-side participation first, DeWi protocols build sufficient infrastructure to attract demand-side users.

Why Solana for DeWi?

Unmatched Network Performance: Solana is renowned for its high throughput and low latency. It can process over 2,600 transactions per second (TPS), and transaction fees are typically less than $0.001. This performance profile is well-suited for DeWi networks, which require efficient handling of numerous micro-transactions and real-time data exchanges

Helium's Migration Success Story: The Helium Network, a leading DeWi project, migrated from its proprietary blockchain to Solana in April 2023. This transition enabled Helium to mint nearly one million hotspots as NFTs using state compression and to leverage Solana's innovative contract capabilities. The migration has been cited as a significant upgrade, enhancing the network's scalability and functionality

Purpose-Built Token Infrastructure: Solana's support for compressed NFTs and programmable NFTs facilitates efficient identity and credential management for devices within DeWi networks. Additionally, Solana's token extensions allow for specialized reward distribution mechanisms, which are essential for incentivizing participation in decentralized networks.

Mobile-First Integration: Solana has ventured into mobile integration with its Solana Mobile Stack (SMS) and devices like the Solana Saga phone. This initiative aims to provide a seamless mobile experience for decentralized applications, potentially offering DeWi projects a direct channel to crypto-native users.

Institutional Support: The Solana Foundation actively supports DeWi initiatives through dedicated hackathon tracks and targeted grants. This institutional backing underscores a commitment to fostering innovation and providing resources for projects aiming to build decentralized wireless infrastructure.

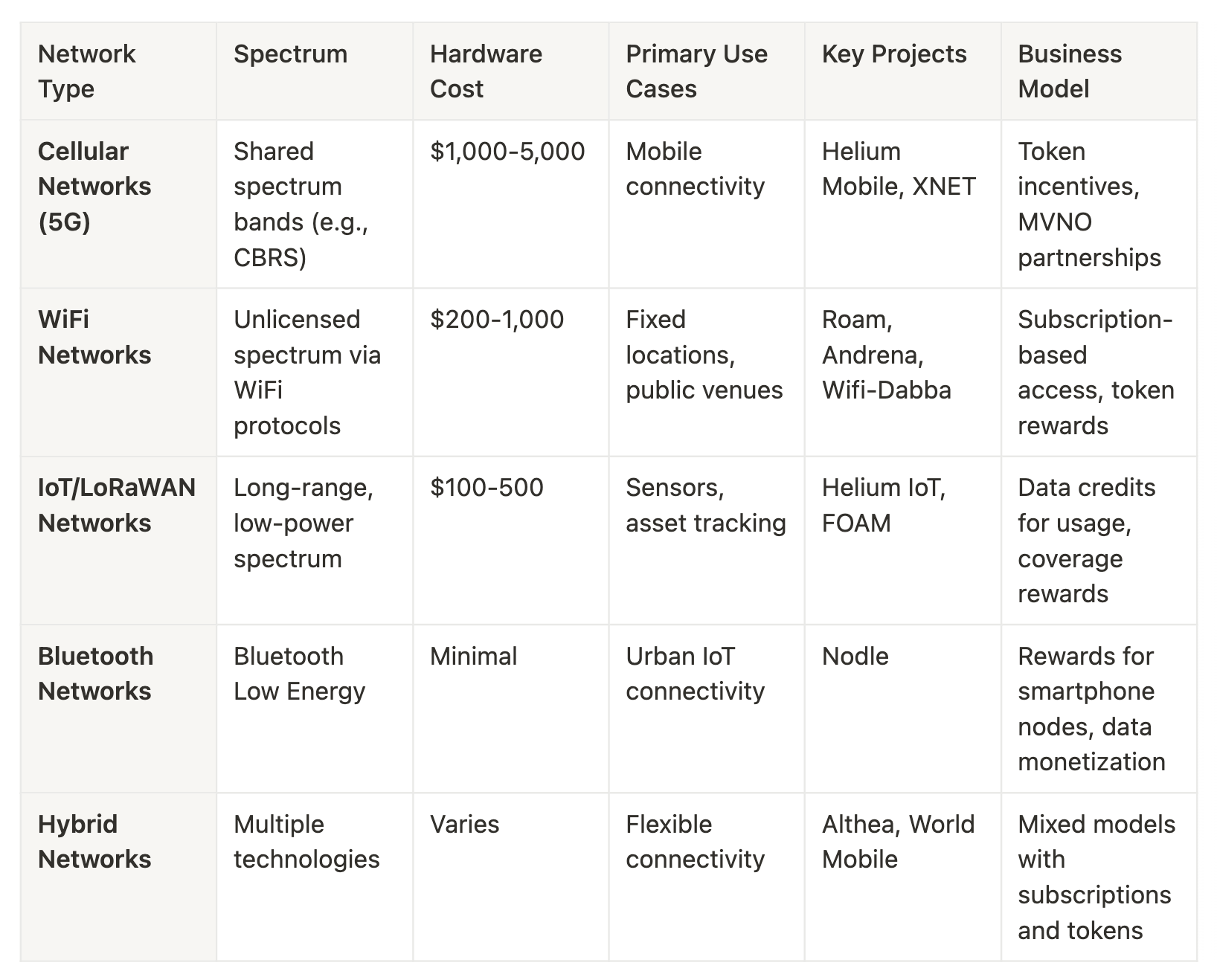

Market Taxonomy: DeWi Network Categories

Market Taxonomy: Competitive Landscape

While all DeWi projects share the fundamental goal of democratizing wireless infrastructure, they've adopted distinctly different strategies to capture market share:

Business Model Spectrum

Pure Token Models (Helium): Rely primarily on token economics to drive network growth and sustainability.

Hybrid Revenue Models (Andrena): Combine traditional subscription revenue with token incentives, creating immediate cash flow.

Carrier-Focused Approaches (XNET): Position as complementary infrastructure for existing telecom players rather than direct competitors.

Target Customer Focus

Consumer-Direct (Andrena, Helium Mobile): Focus on providing connectivity directly to end users.

Enterprise/Carrier Services (XNET, Helium IoT): Target businesses, IoT manufacturers, and traditional telecoms as primary customers.

Dual-Track Approaches (Helium): Pursue both consumer and enterprise adoption simultaneously.

Each strategic approach comes with distinct advantages and challenges, suggesting that multiple DeWi networks can coexist and even complement one another in the broader connectivity ecosystem.

Key Players Analysis

1. Helium Mobile

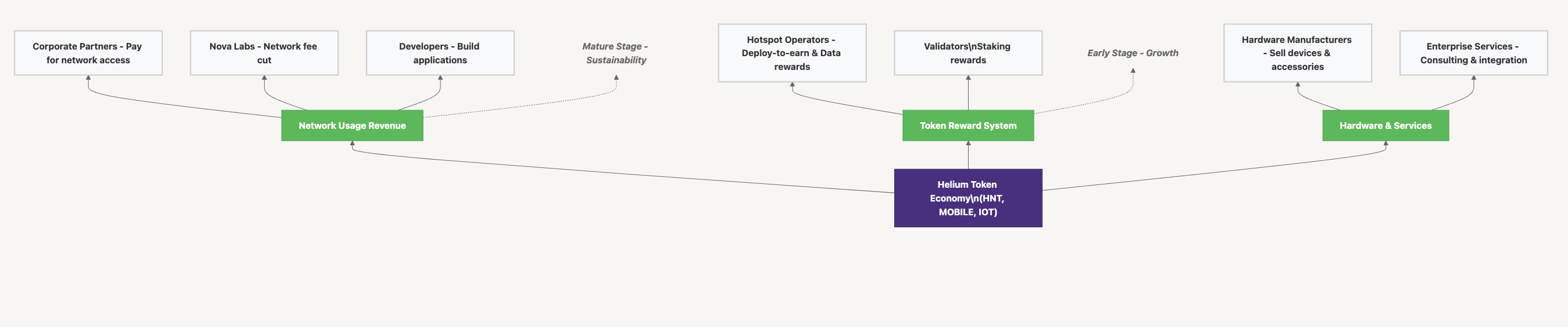

The Helium Network powers two distinct wireless networks: a global LoRaWAN™ network for IoT devices, and a cellular offload Wi-Fi network for mobile connectivity. Wireless gateways called "Hotspots", operated by the Helium community, provide the coverage for these networks. Hotspot owners are incentivized with the Helium HNT token for providing coverage and handling wireless traffic.

Business Model: Helium operates on a "deploy-to-earn" model where participants purchase compatible hardware to build out wireless coverage and earn token rewards. The ecosystem encompasses three distinct networks:

LoRaWAN Network (IOT): The original Helium network facilitates Internet of Things connectivity through low-power, long-range communication.

5G Network (MOBILE): Cellular coverage with CBRS-band compatible hotspots.

WiFi Network (WIFI): The newest addition focuses on public WiFi access points.

The network monetizes through actual usage, with clients paying for data transfers and rewards distributed to hotspot operators based on coverage quality and utilization.

Token Mechanics: HNT serves as the ecosystem's main token, with a burn-and-mint equilibrium that allows supply to respond to network usage trends:

Hotspot operators earn network tokens (IOT/MOBILE) redeemable for HNT

Enterprises pay with Data Credits (DC), a USD-pegged utility token derived from burning HNT

This creates a sustainable economic cycle where usage drives token value

Geographic Focus: Helium has achieved global deployment with over 950,000 hotspots worldwide, with particularly strong presence in:

North American metropolitan areas

Western Europe (Germany, France, UK)

Growing presence in

theAsia-Pacific regions

Traction to Date:

Nearly 1 million hotspots deployed globally

Partnerships with Dish Network, GigSky, and Actility

Migration to Solana has improved transaction speed and reduced costs

2. Andrena

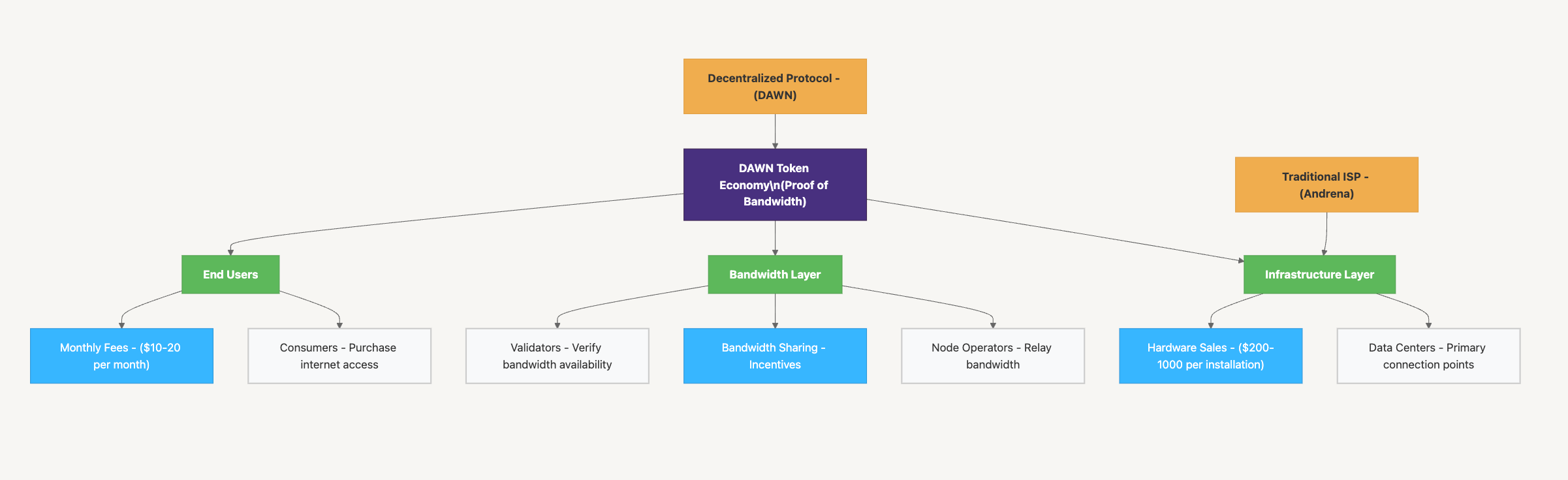

Andrena focuses specifically on affordable last-mile internet connectivity through its Decentralized Autonomous Wireless Networks (DAWN) protocol.

To understand Andrena, a basic understanding of how the Internet works and how connectivity is provided to individuals is required. This process consists of 3 tiers:

Tier 1: This includes subsea fiber optic cables and data center interconnections.

Tier 2: Regional fiber providers like Crown Castle.

Tier 3: Local distributors like Andrena, Comcast, and Verizon. These providers distribute internet within specific markets or regions.

Business Model: Andrena operates with a dual-pronged approach:

Traditional Model: As a Tier 3 internet service provider, Andrena arbitrages the cost difference between wholesale internet prices and retail consumer rates. Their advantage comes from beaming data directly from data center rooftops to consumers.

DePIN/Crypto Model: Through the DAWN protocol, users:

Install antennas (initial cost: $200-$1,000)

Pay minimal monthly fees ($10-$20 versus traditional $100)

Share excess bandwidth with others in the network

Participate in "Proof of Bandwidth" validation

Earn token incentives for contributing to network growth

This approach creates an 80-90% cost reduction for end users while establishing infrastructure only where demand exists.

Geographic Focus: Andrena has established a presence across:

10 different states in the US

Urban and suburban areas where traditional ISP costs are high

Regions with accessible data centers for connectivity beaming

Traction to Date:

Serving over 10,000 households across 10 states

Recently raised $18 million led by Dragonfly Capital

Established profitable operations as a traditional ISP before layering on the DAWN protocol

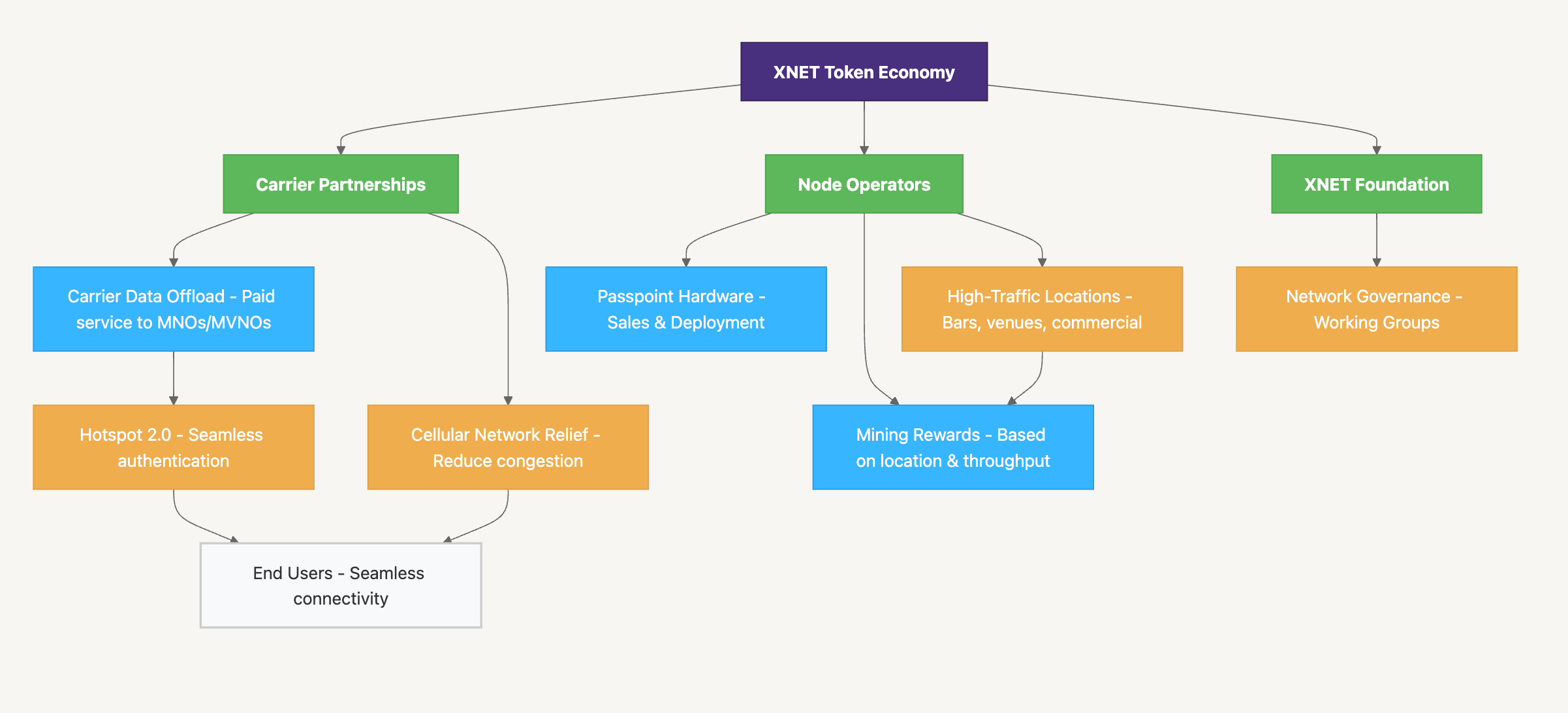

3. XNET Network

XNET is a neutral-host network that works with any carrier, offering cost-effective data offload solutions for both Mobile Network Operators (MNOs) and Mobile Virtual Network Operators (MVNOs).

Business Model: XNET operators deploy "Passpoints" (nodes) in high-traffic areas, which:

Utilize Citizens Broadband Radio Service (CBRS) spectrum

Incorporate Wi-Fi 6+ technology

Support Hotspot 2.0 for frictionless authentication

Enable cellular data offloading without manual logins

Operators earn $XNET tokens based on multiple factors, including hardware specifications, uptime performance, data throughput, and strategic location value.

Geographic Focus:

Operational throughout the United States for paid carrier offload

Available in select Canadian locations for proof-of-coverage rewards

International expansion planned for 2025

Focuses on high-footfall, long-dwell environments valued by carriers (businesses, venues)

Traction to Date:

Approximately 1,200 active nodes deployed

Successfully deployed Hotspot 2.0 technology for seamless carrier offloading

Built by a team of mobile network technology and operations veterans

XNET distinguishes itself by focusing on carrier partnerships rather than building a consumer-facing alternative network. Its emphasis on strategic deployment in high-value locations potentially creates a more immediate path to revenue through carrier partnerships.

Other Players

World Mobile: A hybrid blockchain telco using AirNodes and EarthNodes to bring affordable connectivity to underserved African regions.

Nodle Network: Turns smartphones into decentralized Bluetooth nodes to power a global IoT connectivity network.

Althea Network: A blockchain-powered ISP enabling communities to build and operate their internet networks with automated, crypto-based billing.

FOAM: Provides secure, decentralized location verification using radio beacons and blockchain.

Roam: A decentralized platform for seamless, global WiFi sharing powered by users.

WiFi Dabba: A low-cost mesh internet provider using laser tech to deliver affordable connectivity in urban India.

Market Size and Growth Potential

Analysis Based on PwC Global Telecom Outlook 2024-2028 Overall Telecom Market

Total Global Telecom Service Revenue (2025): Approximately $1.21 trillion (aligns with PwC projection of $1.14 trillion in 2023, growing at 2.9% CAGR)

Year-over-Year Growth Rate: 2.9% (per PwC report, below inflation rate)

Revenue Distribution by Service Type:

Mobile Service Revenue: Largest component

Fixed Broadband: Growing steadily

Fixed Voice: Declining at -1.8% CAGR

Major Market Segments

1. Mobile Services

Technology Distribution by 2025:

5G: ~4.0 billion subscriptions (approximately 46% of total, on track to reach 64.1% by 2028)

Total Mobile Subscriptions by 2025: Approximately 8.9 billion

2. Fixed Services

Breakdown by Technology (by 2025):

Fiber: Largest and growing component (approximately 700-750 million subscriptions)

Fixed Wireless Access: Fastest growing at 18.3% CAGR, reaching approximately 70-75 million subscriptions (on track for 99 million by 2028)

Total Fixed Broadband Subscriptions: Approximately 1.45 billion by 2025 (on track for 1.61 billion by 2028)

3. IoT and Enterprise Connectivity

IoT Vertical Revenue Growth (by 2025):

Smart Cities (inc. transportation & logistics): ~$29-30 billion

Automotive: ~$26-27 billion

Consumer: ~$22-23 billion

Industrial IoT: ~$19-20 billion

Retail & Payments: ~$12-13 billion

Healthcare: ~$6-7 billion

Energy & Utilities: ~$5-6 billion

DeWi Addressable Market Analysis

Analysis Based on PwC Global Telecom Outlook 2024-2028

Total Addressable Market (TAM)

Maximum Potential TAM: ~$400-450 billion

Represents all wireless connectivity segments where DeWi could technically replace traditional infrastructure, regardless of practical constraints

Serviceable Available Market (SAM)

Realistic SAM for 2025: ~$100-120 billion (25% of TAM)

Serviceable Obtainable Market (SOM)

Conservative SOM (2025): $5-7 billion (5-6% of SAM)

Moderate SOM (2025): $7-10 billion (7-8% of SAM)

Aggressive SOM (2025): $10-15 billion (10-13% of SAM)

Adjusted to reflect the realistic market penetration potential given traditional telco dominance

Market Penetration by Segment

Fixed Wireless Access:

Total FWA Market (2025): ~$25-30 billion (based on FWA being 6% of broadband by 2028)

DeWi Capture Potential: 8-12% ($2-3.6 billion)

Rural/Underserved Mobile Markets:

Total Addressable: ~$40-50 billion

DeWi Capture Potential: 3-6% ($1.2-3 billion)

IoT Connectivity:

Total IoT Connectivity Market: ~$10-12 billion (based on PwC showing connectivity as a small portion of overall IoT revenue)

DeWi Capture Potential: 8-15% ($0.8-1.8 billion)

Private Networks:

Total Market: ~$2-3 billion (described as "modest global market" in PwC report)

DeWi Capture Potential: 10-20% ($0.2-0.6 billion)

Growth Trajectory

DeWi Market CAGR (2025-2028): 30-45% (compared to overall telecom CAGR of 2.9%)

2028 Projection: $15-30 billion, depending on adoption rates

Key Growth Drivers:

AI integration aligning with PwC's "Building the AI grid" conclusion

Infrastructure sharing models matching telcos' need to find "new ways of creating value from existing revenue flows"

Current DeWi Market Size (2024-2025)

The current DeWi market is approximately $1.5-2 billion in total size, comprised of:

Helium Network: $1.2-1.5 billion

Over 1 million hotspots deployed globally

Monthly revenue generation estimated at $10-15 million

Multi-token model covering IoT, 5G/CBRS, and WiFi networks

XNET: $80-120 million

Approximately 60,000-80,000 nodes deployed globally

Strong presence in Europe and growing in Asia

Focus on LPWAN technology for IoT applications

Pollen Mobile: $50-100 million

Approximately 5,000-10,000 nodes deployed

Focus on CBRS spectrum in the US market

Other Projects: $100-200 million

Various deployment models across different geographies

Specialized use cases in developing markets and rural connectivity

This represents a very small fraction (<0.5%) of the total global telecom market of approximately $1.14 trillion identified in the PwC report.

The current market size is also just 1-2% of the estimated Serviceable Available Market (SAM) of $100-120 billion, indicating substantial room for growth if DeWi technologies can overcome the technical, regulatory, and market adoption challenges outlined in the PwC report.

Emerging Trends and Future Outlook

The DeWi sector stands at a unique intersection of several major telecom industry trends that could accelerate its growth. The industry's shift toward fiber infrastructure and "wireless at the fringes" creates natural opportunities for DeWi networks to fill connectivity gaps. As established telecom providers increasingly focus their capital expenditures on fiber deployment rather than wireless expansion, DeWi networks can capitalize on this investment vacuum.

The emergence of the "AI grid" represents a significant opportunity, as DeWi networks could provide edge connectivity and compute resources in a distributed manner, supporting the growing demand for low-latency AI processing. This aligns with telecoms' interest in AI-driven network optimization, with DeWi potentially offering more nimble integration of AI technologies than legacy systems.

Regulatory shifts, particularly around spectrum liberalization with bands like CBRS, continue to lower barriers to entry. Combined with the widespread adoption of eSIM technology, which reduces carrier switching costs to near-zero, the foundation for DeWi networks to gain mainstream traction is strengthening.

The telecom industry's ongoing challenge with slow growth (2.9% CAGR through 2028) and difficulties raising prices for commoditized services creates an environment where alternative models like DeWi's token-based incentive systems could thrive. As traditional telecoms search for new revenue streams, partnerships with established DeWi networks may become increasingly attractive.

Looking ahead, DeWi networks are positioned to evolve from complementary coverage solutions to potentially significant players in the telecommunications ecosystem, particularly in specialized markets like IoT connectivity, rural service provision, and support for the expanding edge computing infrastructure required by AI applications.